We independently review every app we recommend in our best apps lists. When you click some of the links on this page, we may earn a commission. Learn more.

As a small business owner who has scaled from simple (read: manual) client invoicing to automating the process altogether, I know that your payment processor is the backbone of your customer experience and cash flow. If your processor lets you down, it dings your reliability and reputability right when it matters the most.

Even though Stripe has long been the default choice for online payments, there are more options than ever—and seemingly more crop up every day. If you feel like you've outgrown Stripe or it no longer gels with your workflow, there are plenty of alternatives that might better fit your business model.

Switching payment processing services is a big decision, but then again, finding the right partner can save you thousands in interchange fees or hours in manual tax filing. In this guide, I'll break down the eight best alternatives to Stripe based on countless hours of testing by the Zapier team, plus my own experience using a lot of them with my small business.

The best Stripe alternatives

PayPal for easy payment setup

Paddle for merchant of record services

Adyen for global enterprises

Shopify Payments for eCommerce stores

Square for selling online and offline

Helcim for interchange pricing

PayPal Enterprise Payments for consolidating payment methods

Airwallex for cross-border businesses

What makes the best Stripe alternative?

How we evaluate and test apps

Our best apps roundups are written by humans who've spent much of their careers using, testing, and writing about software. Unless explicitly stated, we spend dozens of hours researching and testing apps, using each app as it's intended to be used and evaluating it against the criteria we set for the category. We're never paid for placement in our articles from any app or for links to any site—we value the trust readers put in us to offer authentic evaluations of the categories and apps we review. For more details on our process, read the full rundown of how we select apps to feature on the Zapier blog.

Regardless of whether you're chasing lower fees or need a better way to handle physical sales, the best apps like Stripe should shine in a few key areas. To narrow down the best Stripe competitors, I evaluated dozens of platforms based on the following criteria:

Pricing structure: Does the app offer flat-rate, interchange-plus, or subscription-based pricing? It should, at the very least, offer a transparent, scalable model that doesn't balloon your costs when you process more transactions.

Functionality and capabilities: Does it support recurring billing, physical POS (point-of-sale), or MoR (merchant of record) services? A top contender needs to handle the heavy lifting of compliance and administrative read tape so you can focus on growth.

Integrations: How well does it play with your tech stack? No silos allowed for your payment data. A good processor should offer developer-friendly APIs, native connections, or Zapier integration that makes it easy to automate your entire revenue lifecycle.

Security: Does it meet top-tier PCI compliance and fraud protection standards? Trust is the foundation of any payment relationship. We're looking for a secure, reliable environment that protects your business while letting your customers feel uninhibited during checkout. Because the only surprise you want at checkout is a coupon code that works.

The best Stripe alternatives at a glance

| Best for | Standout feature | Pricing |

|---|---|---|---|

Easy payment setup | One-click Guest Checkout for frictionless payments without an account | Free (plus processing fees) | |

Merchant of record | Automated global tax remittance to eliminate international compliance headaches | Free (plus processing fees) | |

Global enterprises | Direct-to-bank acquiring infrastructure for higher authorization rates and faster processing | Free (plus processing fees) | |

eCommerce stores | Native Shop Pay checkout integration for seamless return-buyer conversions | From $29/month, billed annually (plus processing fees) | |

Online and offline payments | Integrated POS hardware ecosystem to unify digital and physical storefronts | Free plan available (plus processing fees); from $49/location/month | |

Volume savings | Automatic volume-based interchange pricing that lowers your rates as sales grow | Free (plus processing fees) | |

Multiple payment methods | Unified multi-walled SDK (Venmo, PayPal, cards) to capture diverse buyer preferences in one integration | Free (plus processing fees) | |

Cross-border businesses | Multi-currency local bank account issuance to collect and spend without massive exchange fees | Free plan available (plus processing fees); from $12/user/month plus a platform fee based on team size |

1. Best Stripe alternative for an easy payment setup

PayPal

PayPal pros:

Instant setup with no lengthy merchant account approval process

Broad adoption supporting hundreds of millions of active users

PayPal cons:

Standard rates can be pricey for high-volume sellers

Historically more buyer-centric in disputes

PayPal is likely the most recognized name in digital payments, which means it has a low barrier to entry for buyers. Lots of people already have PayPal accounts, and its one-click Guest Checkout makes the experience incredibly smooth.

On the seller side, unlike Stripe (which often requires a developer to customize the checkout flow fully), you can set up PayPal's standard integration in minutes. You aren't wrestling with API keys and webhooks just to get a buy button on your site.

PayPal also recently doubled down on its buy now, pay later (BNPL) options, allowing small businesses to offer financing to their customers without taking on the credit risk themselves. This is a huge win for conversion rates, since your customers can split up payments while you get paid the full amount upfront.

One thing you'll notice quickly is that PayPal is very buyer-centric in disputes. While this does build massive trust with your customers, it can be a bit of a headache for the merchant if a customer files a claim. The fee structure is also rough. PayPal's fees are notoriously hard to parse, and standard rates can be pricey for high-volume sellers, so keep an eye on your margins as you grow. But I'd argue the ease of use and name recognition here outweigh these issues.

While PayPal offers an incredibly smooth checkout experience right out of the box, connecting PayPal to Zapier allows you to push that payment data directly into the rest of your tech stack. You can automatically log new sales in your accounting software or alert your team via chat the moment a high-value payment clears. Discover more ways to automate PayPal to keep your business running smoothly.

PayPal pricing: Free; processing fees start at 2.29% plus a transaction fee based on the payment method

Read more: Stripe vs. PayPal

2. Best Stripe alternative for a merchant of record

Paddle

Paddle pros:

Automatically handles global tax compliance and remittance

One platform handles payments, subscriptions, and tax

Paddle cons:

Paddle handles initial customer billing inquiries, which might feel less personal

Checkout pages are slightly less customizable than a full Stripe API integration

If you're selling SaaS or digital goods, Paddle handles the merchant of record (MoR) responsibilities, meaning it oversees payment processing on your behalf. It automates global tax remittance, which is a huge distinction from Stripe, where you're responsible for calculating and remitting sales tax in every country you sell to.

Because Paddle takes on the legal liability of global VAT and GST, you can focus on building features instead of navigating foreign tax laws. It's like outsourcing your least favorite homework assignment forever.

The catch is that Paddle handles your customers' first billing questions, which can feel a bit detached from your brand. And checkout customization isn't as flexible as Stripe's API-first approach. But for many founders, trading pixel-level control for never having to file foreign VAT forms again is an easy decision. (Design perfection is nice. Tax peace is nicer.)

A processing partner that essentially buys the product from you and resells it to the end customer means all that tax liability stops with them. It's one of the few ways to scale globally without hiring a dedicated accounting firm to manage an international nexus.

Paddle pricing: Free; processing fees start at 5% plus $0.50/checkout transaction

3. Best Stripe alternative for a global enterprise

Adyen

Adyen pros:

Built to handle massive scale without performance dips

Deep support for local payment methods in almost every market

Adyen cons:

Requires significant engineering resources to implement fully

Not suitable for small businesses with low monthly transaction costs

Adyen is an all-in-one payment platform for high-volume, enterprise-level businesses that connects directly to card networks and local payment methods globally, leading to higher authorization rates and lower transaction costs for large-scale operations. If you feel like Stripe is too modular, you'll like Adyen's unified commerce platform, designed for consistency across online and in-person channels.

Adyen is built for companies that need deep data insights into their payment flows and the ability to process thousands of transactions per second. Its direct-to-bank acquiring infrastructure cuts out the middleman, which is why brands like Uber and Spotify rely on it.

But Adyen isn't for the faint of heart or the small-scale hobbyist. You'll need significant engineering resources to implement it fully. It's also not suitable for small businesses with low monthly transaction costs—the infrastructure is built to favor businesses with a massive scale.

If you do have the resources, Adyen is consistent. Whether a customer in Paris is buying something on your website or another is tapping their phone at your pop-up shop in Tokyo, the data flows through one single pipe.

Adyen pricing: Free; processing fees start at $0.13 with a transaction fee based on the payment method

4. Best Stripe alternative for eCommerce stores

Shopify Payments

Shopify Payments pros:

No need to jump between different dashboards to see your sales

Saves you the fee usually added for external processors

Shopify Payments cons:

You can only use it if your store is hosted on Shopify

Like most flat-rate processors, they can be quick to pause accounts for high-risk activity

If your business lives on Shopify, as mine does, Shopify Payments is the most integrated Stripe payment alternative you can choose. While it's powered by some of the same underlying technology as Stripe, it's tailored for Shopify. The main reason to choose it is financial: using it eliminates the extra transaction fees Shopify typically levies on third-party gateways.

The biggest draw for your customers is Shop Pay, Shopify's one-click checkout that drastically reduces friction for returning shoppers. For eCommerce merchants, this integration means that your inventory, shipping, and payments are all synced in real time. That reduces the risk of overselling an item or dealing with data mismatches between your store and processor.

The downside is platform lock-in—you can only use it if your store is hosted on Shopify. Also, because it's a flat-rate processor, Shopify can be quick to pause accounts for high-risk activity. If you're selling suspiciously cheap catalytic converters or DIY tax avoidance kits, you might find their compliance team a bit heavy-handed.

For the average online retailer, though, having orders, abandoned carts, and payment data in a single dashboard instead of jumping between Shopify and Stripe is a huge win.

Connecting Shopify to Zapier allows you to automatically route new customer details into your CRM, track inventory changes across different platforms, or follow up with buyers for reviews. For more info, dive deeper into how you can automate Shopify.

Shopify pricing: Starting at $29/month, billed annually, with processing fees from 2.9% plus $0.30/transaction

5. Best Stripe alternative for selling both online and offline

Square

Square pros:

POS devices are easy to set up and look great on a counter

Simple interface requires very little training for employees

Square cons:

Flat rates can be more expensive than interchange-plus models as you grow

High-volume spikes or high-risk items can trigger sudden account freezes

Square is a payment processing leader for businesses that operate both in-person and online. I'm pretty sure that Square was the first company that opened my eyes to payment processors all these years ago when I swiped my card to buy concert merch from the vendor's phone.

Stripe has made strides in POS hardware, but Square's ecosystem of registers, card readers, and tablets is much more mature and user-friendly for non-technical teams. For a small business owner with a physical boutique and an online shop, Square provides a single source of truth for all revenue.

Square's hardware is easy—you can hand a card reader to a new employee, and they'll figure it out in 30 seconds. Plus, the POS devices are easy to set up and look great on a countertop. It's the rare payment device that doesn't scream "1998 bank lobby."

The downside is that flat-rate pricing often ends up costing more than interchange-plus models once your business starts to scale. Also, much like Stripe, if you have a sudden spike in sales or sell something deemed higher risk, you might run into account freezes. If your daily volume jumps from $5,000 to $50,000 overnight, you should probably expect the compliance team to reach out.

Beyond payments, Square offers built-in tools for appointments, payroll, and loyalty programs. It's a flexible platform for flexible businesses that scales with you from a farmers' market to your tenth location.

Connect Square to Zapier to ensure your omnichannel payment data flows perfectly into your other daily apps. You can automatically add new Square customers to your email marketing lists or log every transaction into your accounting software. Learn more about how to automate Square.

Square pricing: Free plan available (plus processing fees); paid plans start at $49/location/month

Read more: Stripe vs. Square

6. Best Stripe alternative for interchange pricing and volume savings

Helcim

Helcim pros:

Your processing rates drop as your volume increases; no negotiation required

They don't charge for PCI compliance or monthly fees

Helcim cons:

They vet businesses more thoroughly than Stripe, so you can't start processing instantly

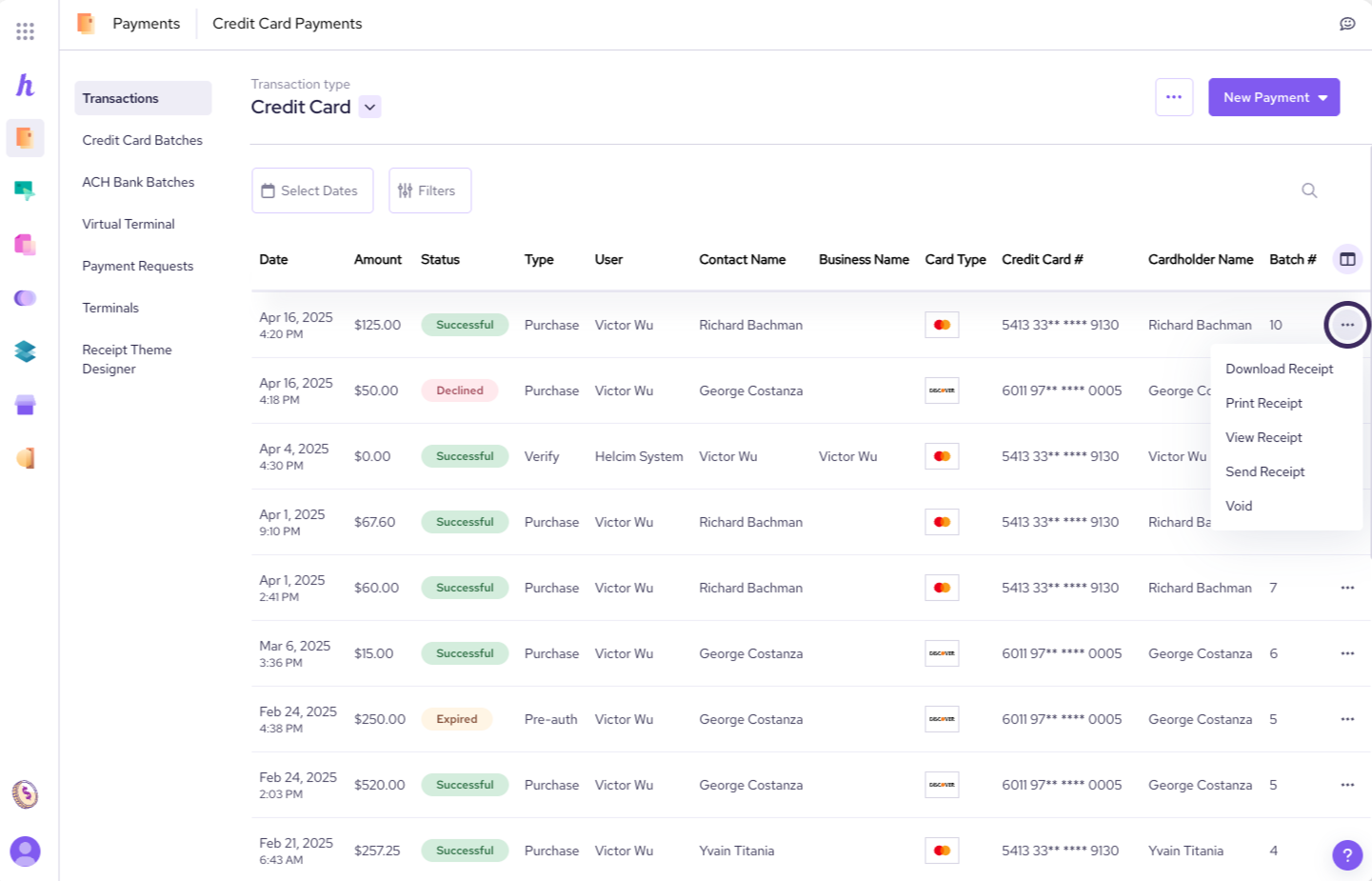

Interchange-plus statements are more detailed and can be harder to understand

Stripe's flat rate can start to balloon if you process a high volume of transactions. Helcim offers an alternative through interchange-plus pricing, meaning you pay the actual cost of the transaction from the credit card network plus a small, transparent fee to Helcim.

As your sales volume grows, Helcim automatically lowers its margin and passes the savings on to you. If your business is established and you have high average order values, Helcim can be much cheaper than Stripe.

The catch is that they vet businesses more thoroughly than Stripe, so you can't start processing right away. They want to know who you are and what you're selling before they open the gates. Also, interchange-plus statements are much more detailed, which can make them harder to parse than simple percentage line items.

Many users love Helcim for its transparency and human-centered customer support. In an industry dominated by chatbots and multi-day wait times, a real person is comforting.

Helcim pricing: Free; processing fees start at 1% plus $0.08/transaction

7. Best Stripe alternative for consolidating multiple payment methods

PayPal Enterprise Payments

PayPal Enterprise Payments pros:

One of the best ways to accept Venmo and PayPal alongside standard cards

Offers robust APIs and SDKs for creating a unique checkout experience

PayPal Enterprise Payments cons:

You'll likely need a developer to set it up correctly

Rates can vary a lot depending on the payment method

PayPal Enterprise Payments, recently renamed from Braintree, is the closest direct competitor to Stripe for developers. Its main strength is its ability to consolidate many different payment methods—credit cards, PayPal, Venmo, and mobile wallets—to capture diverse buyer preferences in a single integration.

Although similar to Stripe, PayPal Enterprise Payments has the added benefit of native integration with the PayPal ecosystem. It feels somewhat like the pro version of PayPal, giving you all the trust of the household name with the flexibility of a modern API.

Be prepared, though: you'll likely need a developer to set it up correctly. Also, rates can vary widely depending on the payment method, which can make your monthly statements a bit unpredictable.

If you're targeting Gen Z or Millennials, the Venmo integration is huge. Customers can pay with a balance they already have in an app they use every day, removing almost all the friction from the buying process.

PayPal Enterprise Payments pricing: Free; processing fees start at 2.19% plus $0.29/transaction

8. Best Stripe alternative for cross-border businesses

Airwallex

Airwallex pros:

Avoid expensive conversion fees by keeping your funds in the original currency

Issue virtual and physical corporate cards with built-in spending limits

Airwallex cons:

Primary strength is in banking and payouts, not retail checkout optimization

Not available in every country, and some features are limited by geography

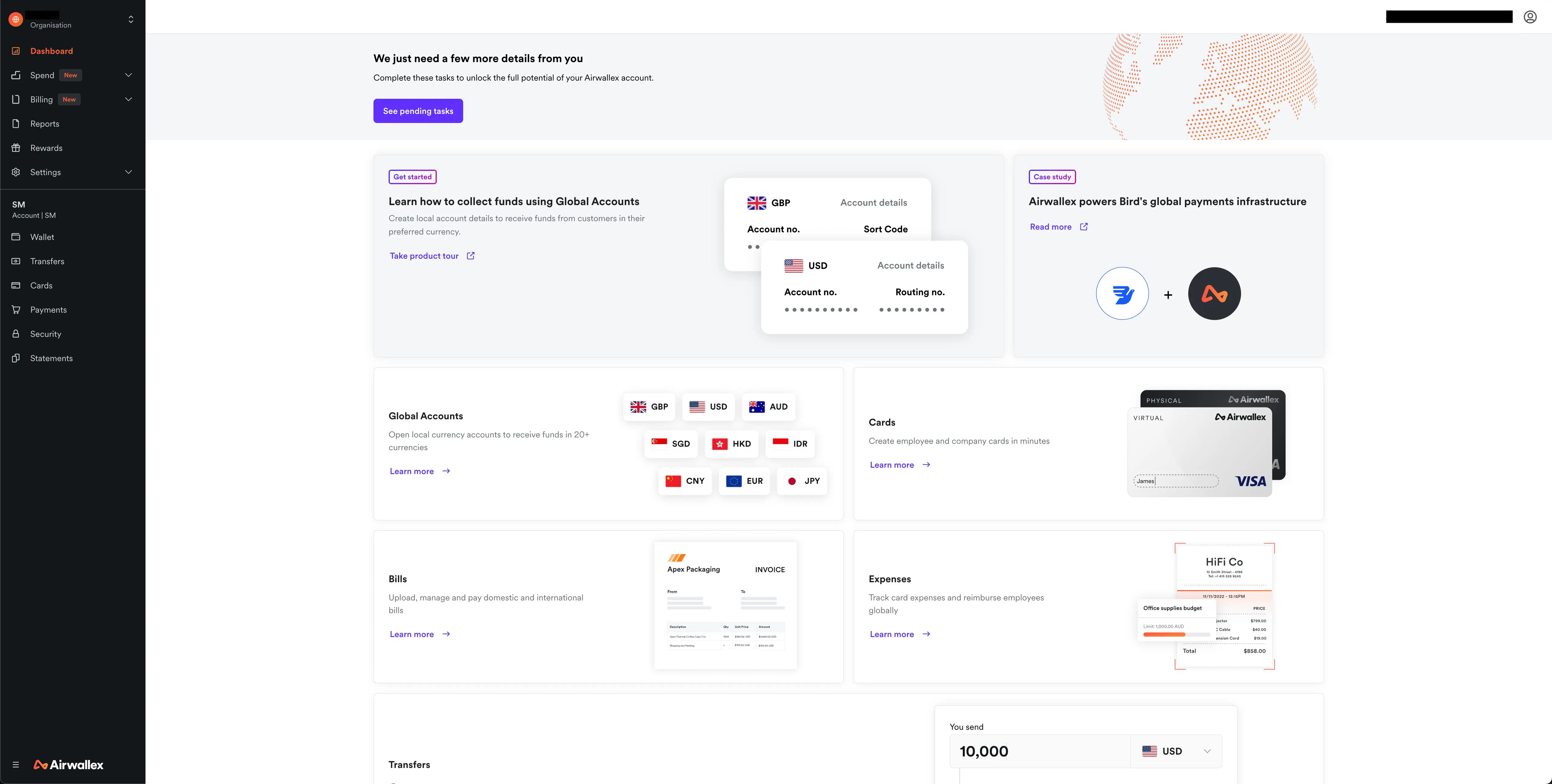

Airwallex goes beyond simple payment processing: it lets you set up local bank accounts in over 11 currencies, so you can collect and spend in local currency without the foreign exchange fees Stripe often charges.

If you have international suppliers, a remote global team, and customers in multiple countries, Airwallex is a financial hub for all of them. It provides virtual cards for your employees and allows for low-cost international payouts.

Airwallex's primary strength is in banking and payouts, though, not retail checkout optimization. If you just want a pretty buy button for your local coffee shop, this is overkill. Also, it's not available in every country, and some features are limited by geography, so check their supported regions before you sign up.

For the international agency or SaaS company, though, the savings on currency conversion alone can fund a new hire. You can collect USD from a customer, hold it in a USD account, and use it to pay a contractor in USD without ever losing 3% to a bank's exchange rate.

When you connect Airwallex with Zapier, you can automatically log international transfers in your accounting database, generate invoices when a local payment is received, or alert your team in Slack when a payout completes.

Airwallex pricing: Free plan available (plus processing fees); paid plans start at $12/user/month

Which alternative to Stripe is best for you?

The best alternative to Stripe is out there, but where is your business today, and where do you plan to be in a few years? If you're a first-time user looking for simplicity and trust, start with PayPal. If you're selling SaaS globally and want to offload the headache of tax compliance, choose Paddle. A brick-and-mortar presence means Square is likely your best bet, while high-volume businesses should look to Helcim or Adyen for savings and stability.

Whichever processor you choose, scaling means freeing your payment data from silos. Zapier connects your Stripe alternative with your accounting software, CRM, and marketing apps so your revenue doesn't live in isolation. Build end-to-end systems in a visual builder, or access your entire tech stack directly from your favorite AI tools.

Related reading: